Determining the Right Price for the Dishes on Your Menu?

Find out how to compare your products on the different dimensions of profitability analysis to make effective decisions - focusing on net margin

You learned in the first part of our series on pricing that there are relevant indicators and calculations that allow you to analyze your costs as well as possible.

Therefore, we have introduced the concepts of cost of goods sold, gross margin, margin on labor costs and finally margin on production costs.

Now let's look at other indicators that will allow you to have a better transparency on your prices and to set them as well as possible.

The operating margin

The operating margin represents the ratio between operating income and sales. This ratio is useful for knowing the long-term viability of your products.

It's calculated as follows: Operating profit / Turnover

As a reminder, the operating sum of your product is equal to the turnover it generates minus the cost of raw materials, supply, labor (in the kitchen and elsewhere), distribution and costs of administrative bodies associated with it.

Net margin by product

The net margin by product, on the other hand, represents the ratio between net profit and sales. This ratio is useful to know the final profitability of your product.

It's calculated as follows: Net profit / Turnover

As a reminder, the net profit of your product is equal to the turnover it generates minus operating profit and corporate tax.

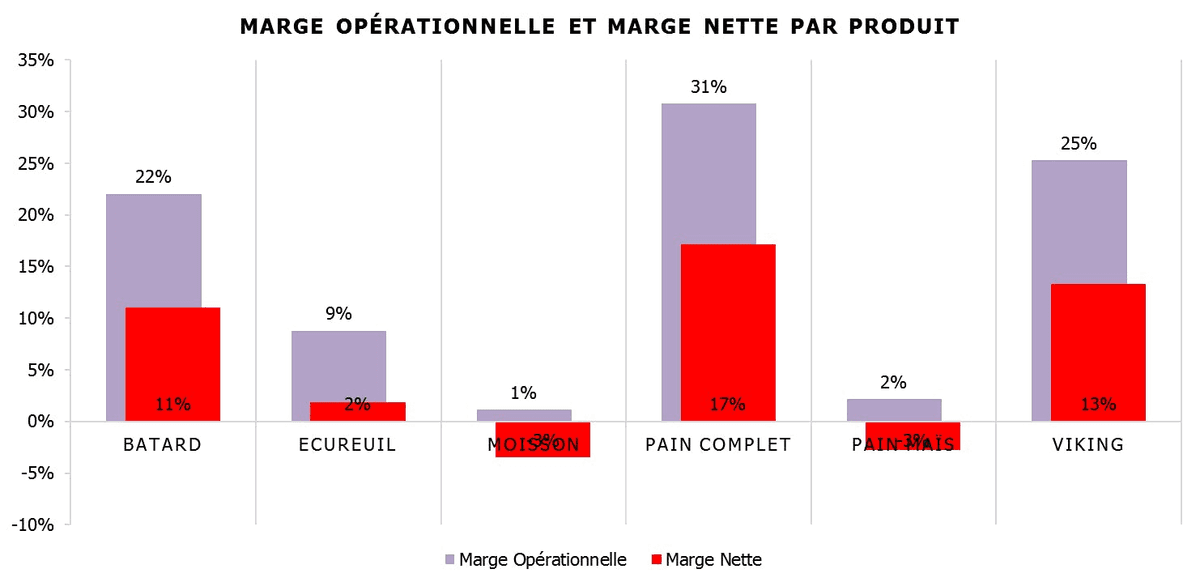

The graph below shows the operating margin and net margin of six breads from a bakery:

A product must maintain a positive net margin to stay appealing.

To be sure, we can play on its price, the cost of its ingredients or the cost of labor. The rest of the costs (labor supply costs outside the kitchen, administrative costs, taxes, etc.) are made up of global charges, which will impact all of your products and not one in particular.

Between the margin on production costs, the operating margin and the net margin, other costs are added: water, electricity, administration, sales, depreciation, borrowing costs, etc.

These costs affect all products uniformly if we do not detail our modus operandi.

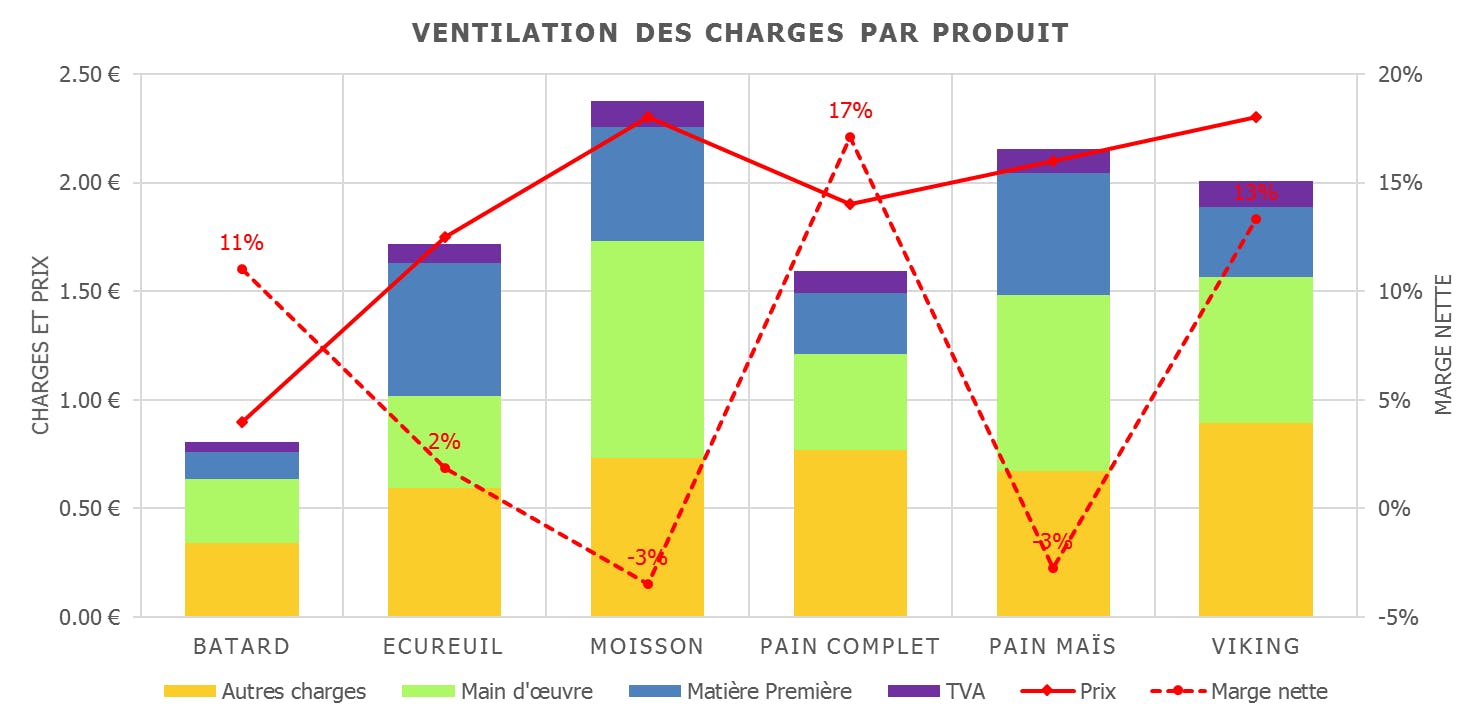

The breakdown of charges

The expense breakdown is a method commonly used to structure cost analysis.

Examine the table below: which products have the least net margin for the baker? How do you fix it ?

If the price curve is below the sum of the costs, the net margin is negative.

Conversely, if the price curve is above the sum of the costs, the net margin is positive.

The “other charges”, in yellow, are the overall charges (such as rent, water, electricity, depreciation allowances, etc.) which will affect all products uniformly. They have an impact on them as a percentage of turnover excluding tax: that is to say that if one of my products represents 20% of my turnover, 20% of “other charges” will be allocated to it.

To increase the profitability of your product, you can work on the price, on the cost of raw materials or on the cost of labor.