Balance Sheet and Profitability: 5 Tools to Improve Your Restaurant's Economic Performance!

Discover some tips that will help you better understand the balance sheet. This will make it easier for you to put in place measures to improve your performance.

In the restaurant sector, as elsewhere, "beginning of the year" is associated with "accounting"! Many have just received their balance sheets and, for some, the economic results may have not lived up to initial expectations.

While the balance sheet is important because it reflects the financial health of your establishment, it's too often poorly controlled and under-exploited. Here are a few tips to help you better understand it. This will make it easier for you to place measures to improve your performance.

1. What is an accounting balance sheet in catering?

The balance sheet is a financial statement which reports the financial state of your restaurant business. You will find:

The assets of the balance sheet are what your establishment has, also called, “jobs”.

Balance sheet assets are made up of tangible and intangible assets belonging to your establishment. Cash, accounts receivable, inventory, machinery, buildings, and the value of a threshold are all examples of your business assets.

The Liabilities of the balance sheet are what you owe to third parties, also called, "resources".

In order to be able to operate assets, the business must acquire them. It therefore owes money to third parties who provide it with the resources necessary to finance the assets. These are the “debts” (example: rents, salaries payable , interest paid to lenders, taxes and duties, etc.). Equity is what is left of the owners' stake in the business, by the difference between the value of assets and the value of debts.

The balance sheet establishes a classification of Assets and Liabilities according to their liquidity. The so-called "current" assets, that is to say the most easily available, are located at the bottom of the balance sheet while the fixed assets are at the top. The same principle is valid for liabilities where debts have a more liquid value than equity.

Whether the operating result is positive or negative, the balance sheet must always remain balanced! The balance between assets and liabilities is maintained at all times because each transaction systematically affects several balance sheet items. It's double-entry bookkeeping.

For example :

- You are a baker , you would like to increase your production capacity and need to buy a new oven. For this, you take out a loan from a bank. This loan will increase your available liquidity (assets) but at the same time, debts will increase (liabilities). When the oven is purchased, the cash will be replaced by a physical asset (your oven).

- You are a restaurateur and you buy your fresh products from your local supplier, payable within 30 days. The value of your stocks increases and at the same time that of your assets. Also at the same time, you have just created a new line of credit with your supplier, this is assimilated with debt. Your liabilities have therefore also increased.

- If you buy these same goods in cash from the same supplier , the asset is impacted twice: once at the level of inventory (which will be credited with the value of the purchase), and the second time at the level of cash that will be depreciated by the same amount. This operation will have zero impact on the value of the total assets and will therefore preserve the balance of your balance sheet!

2. How to identify the economic challenges of your establishment?

The analysis of your balance sheet is done by observing the proportions represented by the major items in this balance sheet. Deciphering the trends behind your financial statement will help you better understand the financial state of your restaurant and allow you to make the right management decisions!

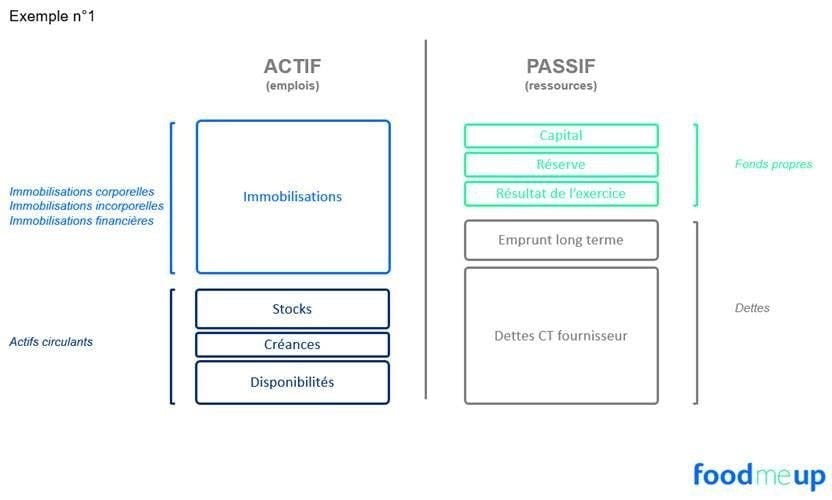

Lets take the 2 examples of balance sheet shown below:

The restaurant in example 1 appears to be in economic difficulty. It has a lot of debt to its credit. They are much larger than liquid assets (inventories + trade receivables + cash). In addition, this restaurant has very little availability. This situation does not allow for all its debts to be repaid.

A more in-depth analysis would be to examine the debts in detail. Here, the ambition is to share the major trends allowing a better understanding.

In example 2, the structure is kept the same for the assets but the liabilities don't have much debt.

It is much less worrying than the previous situation because the short-term debts seem absorbed by the receivables and the availabilities come to add a cushion of liquidity safety.

At this stage, it's good to know that a more precise management of the goods, necessary for your accompanied production, and a better forecasting of the quantities to be produced, will have a positive effect on several items on your balance sheet.

Good calculation will reduce your inventory of goods, increase your liquidity, reduce your payables and improve the result of the financial year.

Click below to find out more on ratios and indicators “Ratios and indicators to follow for a restaurateur, caterer or baker”.

3. The 5 indicators to improve your economic performance

Solvency Ratio

The financial autonomy ratio measures the degree of importance of internal financing compared to total financing. It is expressed as a percentage and in general it's better if it amounts to at least 20% of the total balance sheet.

Financial autonomy ratio = Equity / Balance sheet total

Debt Ratio

The net debt ratio is a ratio that highlights the weight of a company's debt in relation to its equity. It indicates the proportion of debt with which a company finances itself: external sources (loans and financial debts) and internal sources (partners and shareholders). It therefore indicates the level of solvency of a company and its possible risk of default (in the case of a high ratio).

Net debt = Bank debt (short, medium and long term) + Current accounts of partners - Cash and cash equivalents - Marketable securities

Net debt ratio = Net debt / Equity excluding provisions for risks and charges

General liquidity ratio

The general liquidity ratio measures a company's ability to pay off short-term debts. This mainly concerns its supplier debts, tax debts and social debts. It requires calculating two intermediate aggregates: current assets (stocks + trade receivables) and current liabilities (supplier debts + tax debts + social debts).

General liquidity ratio = Current assets / Current liabilities

Working Capital

Working capital corresponds to all the resources made available to the company for a long enough period by its partners, financing organizations, investors, or created through the operation of its activity which are intended for finance, as a first step, for investments in durable goods.

Net Working Capital Requirement (NWCR) = Stable resources - Sustainable jobs

With stable resources = share capital + reserves + profit + associated blocked current accounts + financial debts greater than one year + provisions for risks and charges + depreciation and long-term uses = gross fixed assets

Working capital is positive when stable resources exceed lasting uses. In this case, stable resources fully finance sustainable jobs. The surplus will finance the WCR (in whole or in part) and the balance will help to form the company's net cash. This is a "financial mattress". Working capital is zero when stable resources and sustainable jobs are equal. Here, the resources cover the jobs without a surplus being generated. The company will have to finance its working capital with a bank overdraft for example. Negative working capital is the most critical situation for the company: sustainable investments are not fully funded by resources of the same nature. The financing structure is unbalanced and, if the working capital does not translate into working capital resources, this impacts the net cash flow and the solvency of the company. The company is under-capitalized.

Small tips to improve your working capital

The share of fixed assets in your assets is the main advantage for improving your working capital. In the example of a baker, their cooling chamber and their oven are important items of tangible capital property. The method of financing these fixed assets is therefore strategic. Very often, establishment leaders choose to use their cash to finance their debts. This has the effect of reducing cash and being considered by financial institutions as presenting a high risk. It's generally preferable to finance the fixed asset with long-term debt, which does not endanger the company's liquidity and allows these assets to be settled serenely, at an established pace.

Another lever to improve your Working Capital is to increase your Net Profit. The latter is a direct result of your ability to generate margin on each service and product sold.

Working Capital Requirements (WCR)

The working capital requirement, more commonly known as WCR, is a very important indicator for companies. It represents the short-term financing needs of a company resulting from cash flow lags corresponding to disbursements and receipts linked to operational activity. The working capital requirement (WCR) represents the amount that a company must finance in order to cover the need resulting from cash flow lags corresponding to disbursements (expenses) and receipts related to its activity.

WCR = Current assets - Current liabilities = Average outstanding trade receivables + Average stocks - Average outstanding supplier debts

If the amount obtained by this calculation is negative, the WCR represents a resource for the company; we are talking about a working capital resource. This is particularly the case for catering (where collections are generally made in cash while suppliers are paid at the end of a payment period)

When the WCR is greater than 0, operating uses are greater than resources of the same nature. The company must then finance its short-term needs either by its working capital or by short-term financial debts (current bank overdrafts). When the WCR is equal to 0, the operating resources make it possible to cover the uses in full. The company has no financial need, but it has no financial surplus. When the WCR is less than 0, the uses are lower than the resources. No financial need is generated by the activity and the excess resources released will help to feed the net cash flow of the company.

Small tips to improve your Working Capital Need

Restaurateurs, caterers, bakers: improve your economic performance through actions on stocks of goods!

The stock of goods impacts the Working Capital Requirement since it corresponds to the purchases of ingredients already made, which are waiting to be sold or used in production. Its optimization is all the more important since these goods often have a use-by date which greatly depreciates the value of this stock.

The larger the stock in your restaurant, the more its working capital requirement increases. The following measures allow you to act accordingly:

- optimize stock management to avoid surpluses, dormant stocks, obsolete products

- strive as much as possible towards a "just-in-time" operation (I plan my production and I buy only what I need), so that the company has only the strict minimum in stock

Improve your profitability through actions on trade payables

Trade payables also have an impact on WCRs. The money owed by the company to one of its suppliers corresponds to cash still in its possession, which therefore reduces its needs.

The longer the supplier payment deadlines, the more the company improves its working capital requirement. It's therefore important to:

- negotiate longer payment terms with your suppliers

- improve supplies in order to avoid receiving supplier invoices too early

Net cash (NC)

Net cash is all the sums of money that can be mobilized in the short term (we also speak of cash on sight). It's an indicator of the financial health of a company since it takes account of the balance (or the lack of balance) of its financial structure. It's seen as the result of the difference between the overall net working capital and the working capital requirement.

Net Cash = Working Capital - Need for Working Capital

When the amount of net cash is greater than 0 , a company's resources make it possible to cover all of its needs. The financial situation of the company seems healthy given that it is able to finance new expenses without having to recourse to an external financing method (borrowing for example). It therefore has liquidity that can be mobilized in the short term, but this good news must be put into perspective. Furthermore, it can be the result of a policy of transfer of the productive apparatus or of an investment deficit which can cause difficulties later.

In the case of zero net cash , the resources come to cover the needs to the nearest euro. The company has no room for maneuvre although its financial situation is in balance. The working capital finances the WCR identically and any increase in the latter (lengthening of the payment period for customers, reduction of the payment period for suppliers, increase in the period of stock turnover) will lead the company to encounter difficulties of cash.

If net cash flow is negative , the business does not have sufficient resources to meet its needs. Its financial situation is in deficit and it must absolutely resort to short-term financing methods to remedy this situation (bank overdraft). This situation can only be temporary and represents a real danger for the company if it becomes structural: it portends a risk of bankruptcy.